MasterCard Changes Tack on a Future without Cash

Tuesday, April 06, 2021

Mastercard is hardly perceived as a company supporting cash. In 2006, the company financed an advertising campaign in the UK boasting “Cash Stinks”. In a 2017 interview with Forbes, Banga declared “My enemy is cash, not an electronic payment. Eighty-five percent of the world’s retail payments are still in cash. Paypal and Mastercard and Visa are working only in that remaining 15%.” Mastercard is also a member of the Better Than Cash Alliance which claims that ‘Shifting these payments from cash to digital has the potential to improve the lives of people on low income, particularly women.”

In an October 2020 interview with TED journalist Whitney Pennington Rodgers, Banga discusses financial inclusion, the digital divide and the future of money. He argues that some of the advances made over the past decades in terms of the fight against poverty and exclusion have faced setbacks following the pandemic. Covid-19 has also increased inequality by impacting minorities and disadvantaged people more severely.

Banga also makes several interesting comments on the future of money.

CASHLESS, ACTUALLY, IS SOMETHING WE ARE NOT GOING TO GET TO, AND WE PROBABLY SHOULDN’T

First, Banga recognises that cash will not and more importantly should not go away. “I think cashless, actually, is something we are not going to get to, and we probably shouldn’t.” He rightly points out that there are people who rely on cash because they are unbanked or underbanked, because they are on the wrong side of the digital divide or because they lack a formal proof of identity. Even Sweden sees a need to guarantee access to cash to the most vulnerable. But there are also those who simply prefer to use cash. This group includes Banga’s late father.

REDUCING CASH IN THE ECONOMY IS TO ME A GOOD OBJECTIVE

Secondly, he still believes in reducing the share of cash in the economy. “Reducing cash in the economy is to me a good objective. Taking it to zero? I’m not there.” This is misleading and contradictory. It is misleading because the argument that less cash leads to more transparency and less tax evasion has generated abundant economic debate (Rogoff, Zagorsky, Seitz, Schneider) without any evidence that cash drives the shadow economy. It is contradictory because if digital money is better than cash, then there should be no need for policy measures or commercial incentives to reduce cash usage. The substitution would occur naturally. It isn’t.

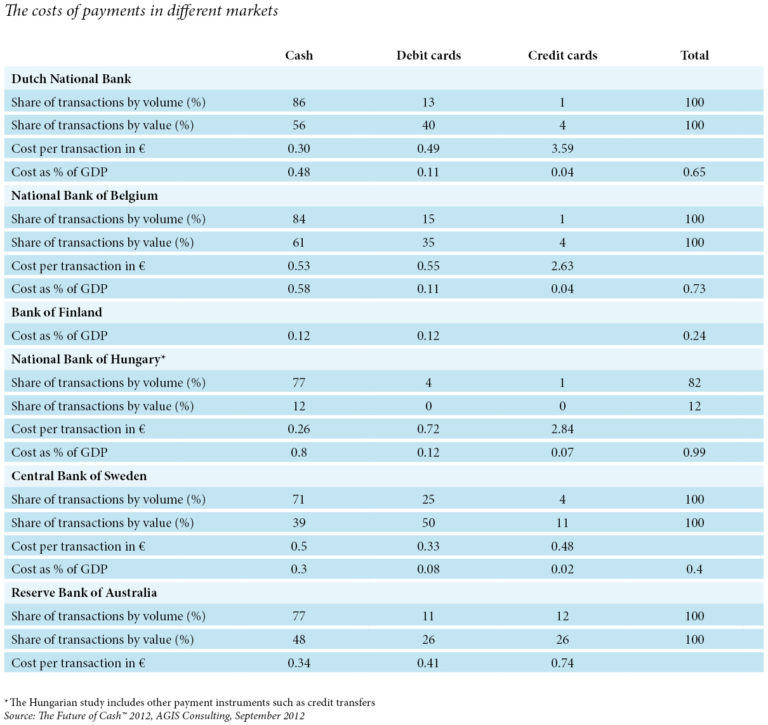

THE COST OF CASH ARGUMENT

Thirdly, the issue of cost of cash in society is put forward as an argument to reduce the relative role of cash in the economy. “One to two percent of GDP.” Says Banga. This is simply wrong. A number of central bank studies have looked into the social costs which vary from 0.12% of GDP in Finland to 0.58% in Belgium. A 2019 Deutsche Bundesbank study found that the average cash payment costs €0.24 vs €0.33 for a girocard and €0.97 for a credit card. A separate academic study found that across 52 countries, the average cash transaction costed $0.54 vs $1.52 for a debit card transaction. One study finds that the aggregate cost of cash in the US amounted to $200 billion (or 1.2% of GDP). Half of the costs are attributed to lost tax income.

CASHBACK IS A SOLUTION

Fourthly, Banga raises the issue of access to cash when the traditional distribution infrastructure, including ATMS and bank branches, is shrinking. He rightly points out that cashback – a service whereby the customer pays electronically a higher amount to a retailer than the value of the purchase for goods and/or services and receives the difference in cash – could provide a solution. Card schemes could in this case become part of the solution as cashback requires a fair business model to work. Retailers should be compensated for the service they provide rather than pay a commission to card schemes. Initiatives have been welcomed in some countries, but it is high time they be extended globally.